Clever mechanics that sidestep the Sebi rules for IAs

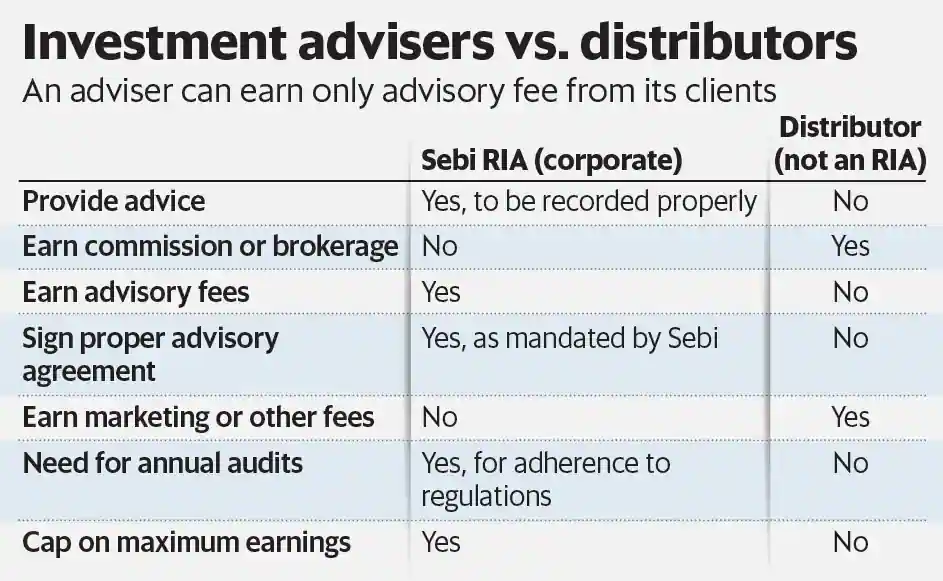

The pure intent of Sebi’s Investment Advisers (IA) regulations is to ensure that clients get the best investment advice without any conflict of interest. Here’s the gist of the regulations, first implemented in 2013 and amended over the years:

An IA must get registered before providing any advice to investors; IAs can only earn advisory fee from clients. They cannot take any commissions, brokerage, referral fees, facilitation fees, etc.; if a client signs up as an advisory client, then the advising entity and the whole corporate group that the IA is part of cannot earn any commission, brokerage or sales fee from either the client or the family/group of the client; any intermediary that does not have the IA certification cannot provide investment advice in any format.

Many product distributors, be they wealth managers, brokers, etc., have been wary about becoming IAs as they cannot earn product or placement commissions that get them anything between 1-5% depending on the type of products sold. But with increasing demand for ‘advisory’ services, some clever mechanics have come into play to cater to investors seeking them. Here are a few:

Portfolio management service (PMS) advisory: Using this route does not explicitly prohibit the intermediary’s owner group to earn product commissions by selling third-party products to the client. Also, while the PMS manager may choose to invest in the direct option of mutual funds, it will not have access to lower fee options in PMS & AIF (alternate investment fund) which are only available to registered investment advisors (RIAs). It is needless to say then that this route is not heavily regulated.

Pushing in-house products: This is the most common practice wherein the IA uses group-manufactured products to earn management fees, operations fees, and the like and also a carry or profit share which can total up to 1-4%. In all these cases, the advisor may even charge a seemingly ‘low’ advisory fee.

The AIF route: While the AIF platform was launched to offer higher risk or alternate funds, the platform has lately seen all sorts of structuring including using pure debt or long-only equity strategies which do not conform to the ‘A’ in AIF, that is, alternative. But even then, we have seen a series of listed equity and mixed asset allocation products. This platform can be used as follows:

One, the advisors use a ‘model portfolio’ AIF scheme to allocate a very large part of the client’s money — so while they could have done the asset and product allocation at the advisory account level, the same structuring is done inside the AIF which obviously can now charge a management fee of 1-2 %, operations fee and maybe a carry, too. This directly goes against the whole bedrock of the IA regulations. Also, there is no regulation around the fact that the advisor can earn commissions and brokerage while selecting products. Two, the advisor structures a new AIF for each ultra high-net-worth individual (UHNWI) – this option sidesteps the IA guidelines and creates a competing structure that has very light regulations, mostly reporting. It does not explicitly bar the intermediary from earning any commissions or brokerage by adding those products into the AIF. It can get worse when the intermediary adds a few in-house products inside the AIF model portfolio!

If investors really need genuine advice, they need to ask questions and not get carried away by the brand, size of the business and other sales tools. One, they need to be sure they are signing up on an investment advisory platform. Two, they need to be conscious and sensitive about any in-house products that are pushed to them. Three, UHNWIs and family offices must ensure that the entity does not have any conflict of interest which might push them to deliver mostly biased advice.

This was originally published in Mint on 01 June 2022